Tom Condon

Published: October 12th, 2023

Updated: April 22nd, 2025

Share this post

Start your property portfolio today!

Should You Invest in a House with Minor or Major Subsidence Issues?

Considering the prospect of investing in a house with subsidence in the UK? The decision to buy a property with subsidence can be a complicated one, as it hinges on the cause of subsidence, potential fixes, subsidence claims, and the involvement of insurance claims.

In 2022, the United Kingdom witnessed a significant number of 23,000 house subsidence claims, highlighting the substantial impact of subsidence issues within the housing market. Troublingly, some sources suggest that nearly 20% of the entire housing stock in the UK is affected by varying degrees of subsidence.

In this article, we’ll cover the details of a house with subsidence, exploring why subsidence occurs, the impact it has on properties, if buying a house with subsidence is a good idea and whether it’s a worthwhile endeavour to invest in homes with subsidence.

Subsidence is the process of ground sinking beneath a property, which can result from either human activities or natural phenomena. While minor ground movement is a common occurrence for homes in the UK, it typically goes unnoticed.

However, when a substantial downward movement occurs, it can lead to houses with subsidence, which in turn jeopardises the property’s stability, structural integrity, market value and eligibility for a mortgage.

Are subsidence and settlement the same thing?

Subsidence and settlement are not the same thing. Settlement usually occurs beneath newly constructed properties when the ground compacts under the weight of the new building. In contrast, subsidence is primarily caused by ground erosion, which directly affects the stability of a home and is not solely linked to the property’s weight.

Do you have to declare subsidence when selling a house?

You must disclose any subsidence issues to potential buyers and insurance providers, even if the property has a history of subsidence. Failing to make this important declaration can lead to some serious consequences.

Notably, your insurer may invalidate your home insurance policy if you do not provide accurate information, leaving your property and investment unprotected.

Furthermore, concealing subsidence from prospective buyers may result in a misrepresentation claim, potentially causing legal and financial complications. Full transparency regarding subsidence is a vital part of selling a house.

How much does subsidence cracks reduce value?

The extent and nature of subsidence cracks can exert a substantial influence on the property’s devaluation, but it’s important to note that subsidence may diminish your home’s market value by as much as 20%.

In practical terms, for a property originally valued at £250,000, this could translate to a significant depreciation of £50,000.

Subsidence can affect properties of all ages, from older listed buildings to new build developments. However, the risk of subsidence is higher for homes built on specific types of soil.

Properties constructed on clay soil, commonly found in the South East of England, are particularly susceptible. Clay soil can expand during wet weather and contract during dry periods, leading to ground subsidence.

Similarly, properties situated on silt, gravel, or sand, such as those near rivers or along the coast are at risk of erosion and subsidence.

Several other factors that contribute to a property’s susceptibility to subsidence include:

The presence of mature and large trees in close proximity to a property can create stability issues with the foundation. Plants looking for water can desiccate the soil, while the extensive roots of large trees may disturb the ground beneath the foundations, making it more prone to movement and cracks.

Areas with a historical record of mining activity are at a higher risk of subsidence. The vibrations from heavy construction equipment or blasting can lead to soil compaction. This is when soil particles are pressed closer together, reducing pore space and has the potential to cause subsidence.

It’s essential to investigate the mining history in the vicinity of a property, especially when considering a purchase in regions like the North West of England, Yorkshire and the Midlands.

Older properties often have shallower foundations that are more susceptible to erosion and subsidence.

The presence of damaged household drains, burst pipes, compromised water mains, or a history of recurrent flooding can elevate the risk of subsidence. Excessively saturated soil can rapidly become unstable and erode beneath the weight of a property.

Are historic and current subsidence the same thing?

Subsidence is often a word that strikes concern in the hearts of potential buyers, but understanding its types and differences can save you a few headaches.

Historic subsidence is generally less severe and refers to cases where a house experienced subsidence in the past, but the issue has since been addressed, with no recurrence. In order for subsidence to be classed as historic subsidence, a structural engineer must have fixed and signed off on the repairs.

If subsidence insurance claims have been part of an insurance claim, it can signify that the subsidence has been completely resolved.

Current subsidence, also known as active subsidence, signifies ongoing and worsening subsidence, which is a more critical concern.

Do you always need a structural engineer when dealing with subsidence?

Regardless of the type of subsidence a property has, whether you are considering the purchase of a property, or have recently acquired one with signs of subsidence, it is imperative that you instruct a structural engineer for an inspection.

The structural engineer will assess whether the subsidence cracks require no additional remediation, or they will provide you with a detailed treatment plan that includes potential costs. This professional evaluation is vital for ensuring the structural integrity and stability of the property.

The average cost of a professional structural survey is around £700 to £1,000 depending on the size of property and inspection. The inspection should tell you if there are any subsidence cracks inside or outside the structure and how you can remedy them.

What are the initial signs of subsidence?

Early signs of subsidence can be identified through a wide range of indicators, if you notice even one or two, we would advise you to seek the advice of a structural engineer. They include:

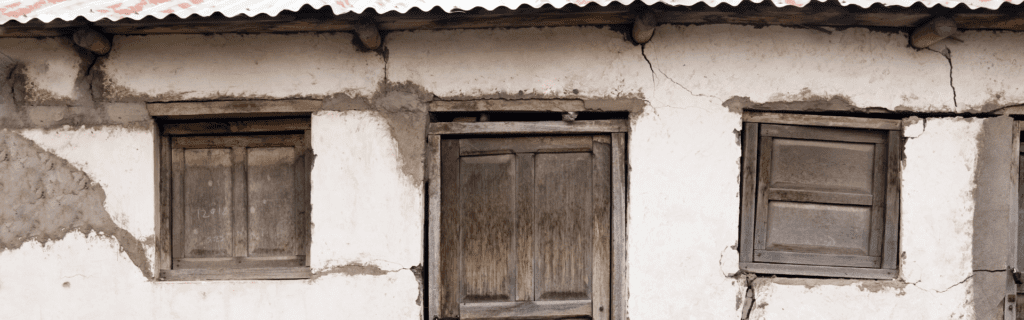

- Cracks in walls, ceilings and floors, particularly around and inside doors and windows which tend to worsen over time.

- Doors and windows may become difficult to operate, sticking or not closing properly.

- Gaps may appear between structural elements of a property like walls, ceilings, doors, windows, and between walls and the floor or ceiling.

- Uneven or sloping floors.

- Bulging or sagging walls or ceilings.

- Unusual marks on external walls like horizontal cracks or deteriorating render.

- Water stains on interior surfaces.

- Wrapping of wallpaper that isn’t caused by dampness.

- Foundation or basement wall cracks.

- Chimney detachment from house.

- Outdoor features such as patios, walkways or retaining walls tilting or sinking.

If you are wondering if buying a house with minor subsidence is a good idea, fear not! Minor subsidence represents a less severe form of subsidence crack, which might not immediately jeopardise a property’s structural integrity. Nevertheless, it’s important to address it promptly to prevent the potential escalation into a more severe subsidence.

What are the signs of minor subsidence?

Minor subsidence can manifest in several ways, such as:

- Hairline cracks, usually measuring less than 3mm in width.

- Slight warping of window and door frames, making them difficult to close.

- Minor irregularities in floor levels.

How is minor subsidence fixed?

If you suspect the presence of a minor subsidence issue, you should consult a qualified structural engineer or Chartered surveyor, who will conduct a thorough property inspection to assess the extent of the damage. The surveyor or engineer will then provide you with a treatment plan, including associated costs.

Usually, addressing minor subsidence problems involves repairing burst or leaking pipes and drains, removing trees and their roots, or enhancing soil quality and drainage around the property.

Once the subsidence has been rectified, continuous monitoring of the property for any further signs of damage or ground movement is advisable.

For properties under 10 years old, you may consider making a claim through the New Homes Building Council (NHBC) scheme, which offers warranty coverage for new build properties.

How much does minor subsidence cost to fix?

Repairing minor subsidence tends to be more cost-effective compared to addressing more severe cases. The expenses vary depending on the specific issue:

- Fixing burst pipes ranges from £50 to £200.

- Hiring a tree surgeon (or arborist) for addressing root removal usually costs around £120 a day.

- Enhancing soil quality falls in the range of £80 to £120.

- Improving drainage around a property can cost around £30 to £40 per square foot.

Fixing major subsidence is similar to fixing minor subsidence, albeit slightly more extensive and expensive. There are three ways to fix most subsidence issues within a property, which your structural engineer will suggest to you within the treatment plan. The subsidence treatment options include:

- Underpinning the foundations

- The cutting back or removal of trees/bushes

- Repairing damaged drains and pipes.

What is underpinning & how much does it cost?

Underpinning is a structural intervention aimed at reinforcing a building’s foundation. This is achieved by utilising long steel piers that are driven deep into the ground beneath the property. These piers serve to lift the foundation, ensuring it is brought back to the correct, level position.

Underpinning is usually the most constant among subsidence treatment options. The price can vary significantly, with expenses ranging from £5,000 to £50,000. The final cost depends on several factors including the size of the property, the extent of damage sustained and the specific underpinning method chosen.

It’s important to note that underpinning, although well-known, is not always the first or most frequently recommended solution for subsidence issues. In fact, according to the Institute of Structural Engineers, only approximately 10% of properties necessitate underpinning.

Due to the extensive scope of work involved, it is often advisable to explore alternative treatments and remedies before resorting to underpinning. This approach not only helps in saving costs, but also ensures that the chosen solution aligns precisely with the unique requirements of the subsidence issue.

How much does removing trees cost?

Tree removal can serve as a more cost-effective alternative to extensive subsidence measures like underpinning. The cost of tree removal varies due to several factors, primarily the size and maturity of the tree in question.

Generally, you can anticipate spending approximately £300 per hour when hiring an arborist to remove a tree. For larger, more mature trees that require 2 to 3 days for removal, the cost can reach around £3,000+VAT.

It’s important to bear in mind that, in rare cases, the removal of trees can lead to a contrary issue known as heave. Heave occurs when the ground beneath a property swells with excess moisture due to the absence of a tree that previously helped maintain moisture levels.

The excess moisture in turn, expands the ground and pushes it upwards, which can lead to the house also being pushed upwards and causing structural damage.

If heave becomes a concern, consulting with an arboriculturist or a tree specialist can offer valuable guidance on addressing heave and mitigating its impact on the property. Usually heave is remedied by reaching down to the sub soils that have not been affected by heave and adding foundations.

How much does fixing damaged drains and pipes cost?

To address damaged drains or pipes effectively, the first step is to conduct a CCTV drain survey. This survey serves as a critical diagnostic tool, enabling professionals to pinpoint the precise location of the issue within the drainage system and formulate an appropriate treatment plan.

The cost of a drainage survey can vary, but you can expect to pay between £45 and £160 for this service. However, the final price you’ll encounter hinges on your location and the severity of the drainage problem.

It depends, if the property has a history of subsidence cracks, it could be a viable option as it may come at a reduced market value. However, if the subsidence issue is ongoing, securing a mortgage might be challenging.

Nevertheless, buying a property with a subsidence history is only a wise decision if you have a full understanding on the problem’s extent, if it is likely to reoccur, any potential additional work required and the associated costs.

It’s worth noting that properties with subsidence issues often sell below their market value, and the cost of remediation can be relatively affordable, depending on the severity of subsidence.

One subsidence has been fully rectified and has received approval from a structural engineer, the property becomes both mortgageable and regains its full market value. Consequently, it may represent a worthwhile investment, potentially offering a lucrative opportunity if you choose to sell it in the future.

What questions should you ask before buying a house with subsidence?

If you’ve found a property that has peaked your interest, but either has subsidence or a history of subsidence, you should ask the homesellers the following questions:

- What is the severity of the subsidence?

- Does the property have ongoing subsidence or a history of subsidence?

- How much will it cost to fix the subsidence and repair the damage it caused?

- Will you be able to get any form of lending, like bridging, on the property to pay for the work?

- Will you be able to get home insurance for the property once the subsidence is sorted?

- Will you be able to easily sell the property in the future once the subsidence issue is fixed?

It’s important to note that alongside asking the home sellers these subsidence questions, you should also get the professional advice of a RICS surveyor or structural engineer who will be able to give you an accurate report of the subsidence.

Can you get a mortgage on a house with subsidence?

Yes, it is possible to obtain a mortgage for a house with subsidence cracks, but certain conditions must be met. To be eligible for a mortgage you will need to demonstrate that the subsidence issue has been fully addressed, and there has been no movement in the past decade.

Keep in mind that finding a lender willing to provide a mortgage for a house with subsidence may be more challenging, but some mainstream lenders possess the expertise to handle such cases.

Navigating the intersection of mortgages and subsidence can be challenging, as each subsidence scenario, whether major or minor, is unique. For the most effective guidance, it’s advisable to consult with a mortgage broker who has experience in resolving subsidence-related issues.

Lenders that do consider offering mortgages for property with subsidence will usually have their own eligibility criteria, which might involve:

- Obtaining a specialised insurance policy.

- Providing a larger deposit to mitigate the potential risk.

- Imposing a cap on the maximum loan-to-value (LTV) ratio.

- Potentially applying higher interest rates.

- Requiring approval from a valuer.

- Furnishing evidence of appropriate warranties or guarantees for any remedial work that has been undertaken.

Is it possible to remortgage a house with subsidence??

Yes, it is feasible, but the process can present some financial challenges. When dealing with a property afflicted by ongoing or historical subsidence, seeking to remortgage with a new lender entails being assessed as a completely new customer, subject to scrutiny regarding your mortgage risk.

Alternatively, you may choose to remain with your existing lender and explore more competitive mortgage products they offer. In either case, you are likely to be required to provide evidence that any necessary subsidence remediation work has been completed.

However, opting to stay with your current lender may offer a more advantageous position compared to attempting to remortgage with a different lender. This is because your existing lender already has a history with your property and may be more amenable to your situation.

Can you get home insurance on a property with subsidence?

Securing home insurance for a house with subsidence is indeed possible, but it’s important to be prepared for potentially higher building insurance premiums due to the potential risks. In many cases, you may find that you need to turn to specialist insurers who are well versed in houses with subsidence.

Moreover, specific policies tailored to address subsidence-related concerns may be required by certain mortgage lenders. In fact, some mortgage providers may insist on these policies as a condition for granting a mortgage.

When should you inform your insurance provider?

For property investors, recognising the signs of subsidence damage is vital when managing a property investment. If you suspect that your property has been affected by subsidence, it’s imperative to promptly notify your insurance provider.

Their guidance is indispensable in swiftly addressing subsidence. In many cases, insurers may dispatch a qualified structural engineer to assess the damage on-site and determine the necessary course of action.

What are the next steps for insurance providers during subsidence?

The subsequent steps hinge on the extent of the subsidence damage. If the damage is minor, and both the cause and movement have been effectively determined and contained, the remediation process can commence without delay.

However, in instances of severe damage or ongoing subsidence, a more thorough approach may be required. In such cases, your property’s movement may be closely monitored over an extended period allowing engineers to devise a long-term solution like underpinning.

What insurance claim cover do you have for subsidence?

It will depend on your policy, but the Association of British Insurers suggests that most building insurance policies will encompass protection for damage inflicted upon the structural elements of your property and any associated outbuildings due to subsidence.

Most insurance policies will come with an excess of about £1,000 for subsidence claims.

Damage to peripheral structures like garden walls, gates, fences, driveways and patios may not fall within the purview of a standard coverage unless this damage occurs simultaneously with the damage to your primary property.

In the event that subsidence damage renders your property uninhabitable, your insurance will often cover the cost of alternative accommodation while essential repairs are underway.

Investing in a house with subsidence is a complicated process, which has the potential to be quite costly, but it could provide a beautiful return on your investment. When looking to invest in a house with subsidence you will need to evaluate your property investment strategy, here are some crucial steps to consider:

- Understand the subsidence cause: Begin by identifying the cause of the subsidence and its severity. An inspection by a structural engineer should provide you with a report on the subsidence.

- Historical research: Delve into the property’s history, particularly regarding its insurance coverage. Properties with a subsidence history may encounter challenges in securing future insurance coverage.

- Risk assessment: Evaluate your risk tolerance, financial capability and your willingness to commit time to the property investment.

One potential challenge for property investors is that selling a house with subsidence on the open market may prove difficult.

Potential buyers often encounter obstacles in obtaining mortgages for properties with ongoing subsidence issues, limiting the pool of prospective purchasers to cash buyers. This can lead to a smaller market, longer sales timelines and potentially lower market values.

However, there are alternative avenues for buying and selling properties with subsidence outside of the open market. If you’d like to explore these options and gain insights into managing properties with subsidence effectively, read the section below…

Large discounts on property

Completely transparent

Tailored investment opportunities

We’ll handle everything for you