BMV Residential Property Investment – What Defines It?

Landlords and property investors alike invest in residential property and rent it out to tenants in order to receive a rental income. But as with any property investment, there are lots you need to consider before taking the plunge and investing in residential properties.

Discounted property with high yields

Transparent & honest throughout the process

We’re property experts with years of experience

Investment opportunities tailored to your requirements

On this page, we will be looking at what is and what is not classed as residential property, why it matters, and what it means for you as an investor.

Are you looking to get into the buy-to-let market and find potential property purchases with great rental yields? That’s something we can help with.

WHAT DEFINES RESIDENTIAL PROPERTY UK?

If you look at the Government website, you will see that residential property is usually defined as “buildings or part of buildings that are to form a dwelling, together with garden or grounds, as well as land intended for such use.” Whereas with the chargeable gains rules, it is not about the use of the buildings, but rather the intended use of the buildings.

To put it in simpler terms, residential property is any unit or building that is zoned and purposed as a living space. Property is usually divided into two main groups, residential and commercial. As a rule of thumb, residential property is typically user-occupied but this is not always the case.

WHAT IS CLASSED AS A RESIDENTIAL PROPERTY?

Residential property includes property or units that have been zoned as living spaces as well as land where construction activities have not yet started but has been planned to start. Signs of this would include planning permission or the marketing of the land with permission by a company with interest in the land that it holds as tracking stock.

Examples of what can be classed as residential properties include:

- Single-family homes

- Multi-family homes of two, three, or four units

- Townhomes

- Semi-detached homes

WHAT IS NOT RESIDENTIAL PROPERTY?

Non-residential property is a property that does not fit in the following criteria:

- A building that is either used or is suitable to be used as a dwelling, or is currently being constructed or adapted for use

- Land that either is or forms part of the garden or grounds of a residential building

- An interest in or right over land that subsists for the benefit of a residential building

Start your property journey today

Start your property journey today

IS A GARAGE CLASSED AS RESIDENTIAL?

Because a garage is classed as part of a building or structure either in the grounds or garden of the property, it is classed as a residential property. This is regardless of the purpose of the property. This means that if you use your garage as somewhere to store your cars or work tools, it will still be classed as residential.

How do I get involved with residential properties for sale?

If you do not have the immediate funds to purchase a residential property that you are planning to let out, then a buy-to-let mortgage is the route for you. A buy-to-let mortgage is ideal for those who are looking to get into the world of property investment. A buy-to-let mortgage will allow you to use the rental income to pay the mortgage whilst providing you with extra income for your own spending.

What costs are associated with residential properties?

When you use a buy-to-let mortgage, it is worth keeping in mind that you will need to pay a higher interest rate and arrangement fees as well as a deposit of at least 25% of the property purchase price.

You will also need to factor in the following:

- Accountant fees

- Solicitors fees

- Stamp duty

- Capital gains tax (only applicable if you sell the property for a profit)

- Repairs and maintenance

- Tenancy and inventory fees

- Buildings and landlords’ insurance

- Estate agents fees

- Annual checks and certificates

- Rental voids and bills

How does Stamp Duty Land Tax affect a residential property sale?

Stamp duty land tax (SDLT) is charged on ‘dwellings’, which UK residential property falls under. If you have a residential property, you will pay stamp duty land tax at a much higher rate than an owner of a non-residential property would. SDLT can be as high as 15% so it is worth knowing:

- If your property can be classed as not being a ‘dwelling’ as being ‘mixed use’ then you can usually expect a lower rate of SDLT will be applied.

- The definition of a dwelling is important when it comes to selling and buying a residential property with multiple occupants. Depending on whether it counts as one or several dwellings, you may be able to access the following:

- – Non-residential rates when acquiring six or more dwellings together

- – Multiple dwelling relief

Start your property journey today

Start your property journey today

WHEN DOES CONSTRUCTION COUNT AS A RESIDENTIAL PROPERTY?

When it comes to SDLT, HMRC does not adopt the same policies that VAT on construction projects can take. Instead of waiting until construction has progressed past the level of foundation, there must be evidence of construction commencing.

If you have multiple dwellings in your property development, then this will be applied to each dwelling sold, and if work has not yet started, then no multiple dwellings relief can be claimed.

If you have a mixed-use development, simply starting construction will be evidence enough to have it classed as mixed-use.

Can land or gardens be taxed?

If you are planning to carve out a plot from your grounds or garden whilst your property is retained, HMRC will typically tax the land as if it were residential. This will be the case, even when the land is fenced off and is physically inaccessible to the vendor or owner. However, it is worth keeping in mind that:

- If the buyer you sold to then sells off that parcel of land, it will have lost its residential nature in the eyes of the then-vendor

- If when you sell the land the property is not a dwelling, then the land will not be considered to be either.

WHAT ARE THE PROS AND CONS OF RESIDENTIAL PROPERTY INVESTMENT?

As with any investment, there are pros and cons to investing in properties of a residential nature. Below we have a look at the advantages and disadvantages that come with it:

Pros of residential property investments

- Demand – Renting is becoming an increasingly popular housing option. As there is high demand for rental properties, now is the time to start investing.

- Income – Another upside to residential investment is that the rental income that you generate should cover your mortgage and other expenses. By renting, you are essentially ensuring someone else pays off your mortgage whilst earning extra income on the side.

- Safe – Whilst it is an accepted fact that house prices will fluctuate, investing in property is regarded as pretty safe and there is the chance to make money on your sale if the property price increases whilst you own it.

Cons of residential property investments

- Tenants – Whilst most of the tenants that you rent your investment home out to should be courteous, there is every chance that at some point you will have to deal with a bad tenant. They are part and parcel of being a landlord and they are something you may have to prepare for.

- Unexpected bills – Unfortunately, expected bills are a part of every landlord’s life and come hand in hand with any investment property. Whilst they shouldn’t be too common, as a landlord it is your job to handle any repairs that need doing in a prompt manner.

- Void – When you are renting out a house, an aspect you will need to prepare for is void periods. This is when the property is vacant but the bills will still need to be paid. At one point or another, you will experience a void, so it is a good idea to have some savings tucked away.

Start your property journey today

Start your property journey today

WHAT BTL OPTIONS ARE THERE?

These tend to be normal residential houses, 2 to 3 bedrooms terrace, semi-detached, detached or flats.

They are houses that are suitable for the average renter and are sometimes known as vanilla buy to let properties.

A House of Multiple Occupancy (HMO) is a rented property occupied by at least three people who are not from one household or five or more people, forming two or more households.

This type of Buy To Let is a freehold block which offers multiple, separate or independent residential units.

This can be a variety of different types of property such as blocks of flats or houses converted into flats.

This is very similar to HMO’s and even are often referred to as non-licensable HMO’s.

They have many characteristics of a typical HMO but don’t require the licence, but they may still require planning permission from your local authority.

As the name describes, this is a commercial premises and it is when you let the property out to one or more businesses.

It’s often referred to as Commercial Landlord Mortgage, Business Buy To Let Mortgage or Commercial Investment Mortage.

OUR LOCATIONS

Thinking of buying a BMV property, but have a specific area in mind? To give you an understanding of just how broad your property choice is, here’s the areas where we most regularly buy BMV property…

Start your property journey today

Start your property journey today

EXAMPLES OF PROPERTY INVESTMENTS

Have we got your interest? Well, how do you know that we’re going to provide great deals? Just take a look at some of our recent sales in the area, they speak for themselves!

Want to see more of our deals? Check out our recent deals.

Buy Refurbish Rent Refinance

Scunthorpe, DN16

House, Semi-detached Freehold

25% BMV

Yield

8.3%

- Freehold

- Driveway

- Rear garden

- Close to local amenities and transport links

- Could achieve £700 – £750 pcm

- Vacant upon completion

Buy Refurbish Rent Refinance

Scunthorpe, DN16

House, Semi-detached Freehold

25% BMV

Yield

8.3%

- Freehold

- Driveway

- Rear garden

- Close to local amenities and transport links

- Could achieve £700 – £750 pcm

- Vacant upon completion

AirBnB

Bakewell, DE45

House, Terrace Freehold

22.1% BMV

Yield

15.2%

- Freehold

- Grade II listed

- £51,000 per annum gross rental

- £200 nightly average

- 70% predicted occupancy

- RICS £420,000 in current condition

AirBnB

Bakewell, DE45

House, Terrace Freehold

22.1% BMV

Yield

15.2%

- Freehold

- Grade II listed

- £51,000 per annum gross rental

- £200 nightly average

- 70% predicted occupancy

- RICS £420,000 in current condition

Refurb to Flip

Tadley, RG26

Bungalow, Detached Freehold

45% BMV

Exit Profit

20%

- Freehold

- Refurb opportunity

- RICS value £300,000

- Strong demand from owner occupier

- Great transport links

- 50 Miles from London

Refurb to Flip

Tadley, RG26

Bungalow, Detached Freehold

45% BMV

Exit Profit

20%

- Freehold

- Refurb opportunity

- RICS value £300,000

- Strong demand from owner occupier

- Great transport links

- 50 Miles from London

Buy To Let

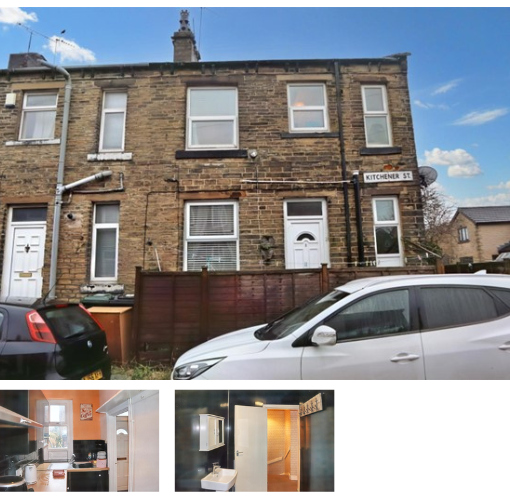

Bradford, BD12 7DE

House, Terraced Freehold

24.3% BMV

Yield

10.8%

- Freehold

- 4.1 Miles to Bradford City Centre.

- 1.5 Miles to M606 & M62.

Buy To Let

Bradford, BD12 7DE

House, Terraced Freehold

24.3% BMV

Yield

10.8%

- Freehold

- 4.1 Miles to Bradford City Centre.

- 1.5 Miles to M606 & M62.

WHY SHOULD YOU INVEST WITH US?

We’ll find you the best deal, with the highest yield possible, tailored to your requirements.

We have years of experience in this industry and are part of a group of companies that regularly purchase properties for below market value, in which we can pass the discount on to yourself. We’ll look at every property we purchase, or even get an enquiry for, to determine if it will offer a high yield. If the answer is yes, we can pass the opportunity on to our investors.

We make it easy, doing all the research for you & finding the perfect property to slot into your portfolio.

WHY SHOULD YOU INVEST WITH US?

We’ll find you the best deal, with the highest yield possible, tailored to your requirements.

We have years of experience in this industry and are part of a group of companies that regularly purchase properties for below market value, in which we can pass the discount on to yourself. We’ll look at every property we purchase, or even get an enquiry for, to determine if it will offer a high yield. If the answer is yes, we can pass the opportunity on to our investors.

We make it easy, doing all the research for you & finding the perfect property to slot into your portfolio.